DJO Global Announces Financial Results For First Quarter of 2013

SAN DIEGO, CA, APRIL 26, 2013 – DJO Global, Inc. (“DJO” or the “Company”), a leading global provider of medical device solutions for musculoskeletal health, vascular health and pain management, today announced financial results for its public reporting subsidiary, DJO Finance LLC (“DJOFL”), for the first quarter ended March 30, 2013.

First Quarter Results

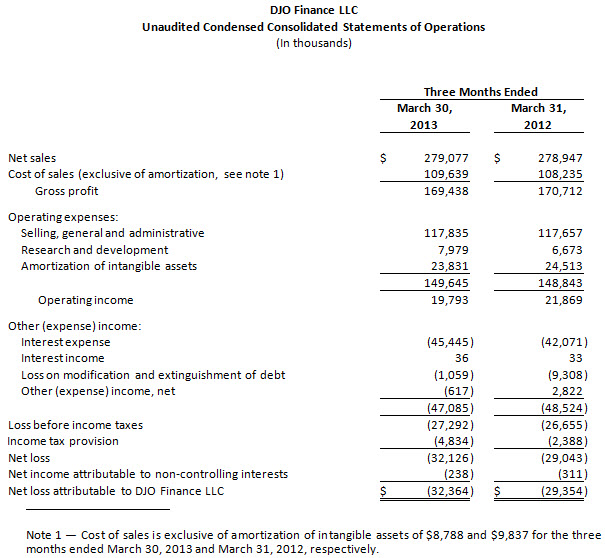

DJOFL achieved net sales for the first quarter of 2013 of $279.1 million, roughly flat with net sales of $278.9 million for the first quarter of 2012. Net sales for the first quarter of 2013 were not materially affected by changes in foreign currency exchange rates compared to the rates in effect in the first quarter of 2012, but were impacted by fewer shipping days compared to 2012. Average daily sales for the first quarter of 2013 increased 1.9 percent compared to average daily sales for the first quarter of 2012. The first quarter of 2013 included 63 shipping days in the United States and 62 days in most international markets, while the comparable 2012 period included 64 days.

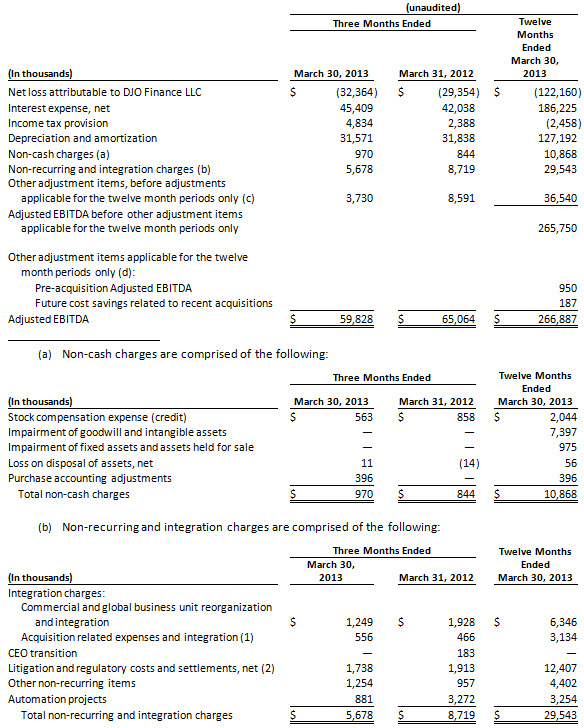

For the first quarter of 2013, DJOFL reported a net loss attributable to DJOFL of $32.4 million, compared to a net loss of $29.4 million for the first quarter of 2012. As detailed in the attached financial tables, the results for the current and prior year first quarter periods were impacted by significant non-cash items, non-recurring items and other adjustments.

The Company defines Adjusted EBITDA as net (loss) income attributable to DJOFL plus interest expense, net, income tax provision (benefit), and depreciation and amortization, further adjusted for certain non-cash items, non-recurring items and other adjustment items as permitted in calculating covenant compliance under the Company’s amended senior secured credit facility and the indentures governing its 8.75% second priority senior secured notes, its 9.875% and 7.75% senior notes and its 9.75% senior subordinated notes. Reconciliation between net loss and Adjusted EBITDA is included in the attached financial tables.

Adjusted EBITDA for the first quarter of 2013 was $59.8 million, or 21.4 percent of net sales, reflecting a decrease of 8.0 percent compared with Adjusted EBITDA of $65.0 million, or 23.3 percent of net sales, for the first quarter of 2012. Adjusted EBITDA for the first quarter of 2013 was not materially affected by changes in foreign currency exchange rates compared to the rates in effect in the first quarter of 2012.

For the twelve months ended March 30, 2013 (LTM), Adjusted EBITDA was $266.9 million, or 23.6 percent of LTM net sales of $1,129.6 million, including pre-acquisition Adjusted EBITDA and expected future cost savings aggregating $1.1 million related to the Company’s recent acquisition of Exos Corporation.

"We were pleased to see all of our business segments except for Recovery Sciences, which has been hampered by market and reimbursement hurdles, perform quite well in the first quarter,” said Mike Mogul, DJO's president and chief executive officer. “I want to especially congratulate our Bracing and Supports, Surgical Implant and International teams, for delivering strong organic growth in the first quarter of 2013. Our Recovery Sciences business has been impacted in recent quarters by Medicare’s 2012 non-coverage decision related to Transcutaneous Electrical Nerve Stimulation (“TENS”) for chronic low back pain (“CLBP”) and slower than expected market conditions for capital equipment purchasing, which is impacting our Chattanooga business.

“For the first quarter, as expected, Adjusted EBITDA contracted modestly from the prior year amounts, due partly to the impact of the medical device excise tax, which became effective January 1, 2013, partly to the recent Medicare CLBP non-coverage decision and partly to increased operating expense investments related to upcoming product launches and other revenue growth initiatives.

“We have a very exciting slate of new products for 2013 that we began launching late in the first quarter. These new products were highlighted at the American Academy of Orthopedic Surgeons meeting in March and were extremely well received. We expect these new products and other ongoing commercial initiatives to drive incremental top line growth beginning in the second quarter of 2013, and we continue to target total company full year revenue growth rates of at least 5%. We continue to expect to absorb the impact of both the Medicare CLBP decision and the new medical device excise tax and still deliver full year growth in Adjusted EBITDA that is at least as high as our revenue growth.”

Sales by Business Segment

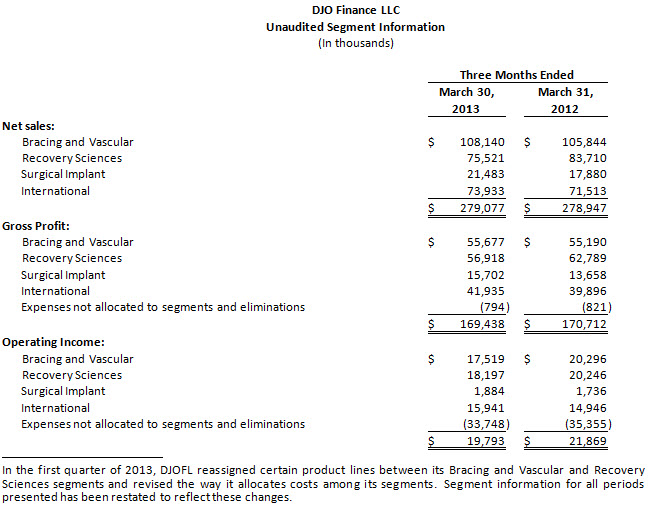

In the first quarter of 2013, DJOFL reassigned certain product lines between its Bracing and Vascular and Recovery Sciences segments and revised the way it allocates costs among its segments. Segment information for all periods presented has been restated to reflect these changes.

Net sales for DJO’s Bracing and Vascular segment were $108.1 million in the first quarter of 2013, reflecting growth in average sales per day of 3.7%, compared to the first quarter of 2012, driven by strong contribution from the sales of new products and improving sales execution.

Net sales for DJO’s Recovery Sciences segment were $75.5 million in the first quarter of 2013, reflecting a contraction in average sales per day of 8.4%, compared to the first quarter of 2012, reflecting the effects of the Medicare CLBP decision on the EMPI business unit, slow market conditions for capital equipment sold by the Chattanooga business and the impact of certain distribution changes on the CMF bone growth stimulation business unit.

First quarter net sales within the International segment were $73.9 million, reflecting an increase in average sales per day of 6.3% from the prior year period, excluding the impact of $0.1 million of favorable changes in foreign currency exchange rates from rates in effect in the first quarter of 2012 (“constant currency”). The strong international growth is being driven by increased penetration in certain geographies and the impact of sales of new products.

Net sales for the Surgical Implant segment were $21.5 million for the first quarter of 2013, reflecting an increase in average sales per day of 22.1% over net sales in the first quarter of 2012, driven by strong sales of each of the Company’s shoulder, knee and hip product lines.

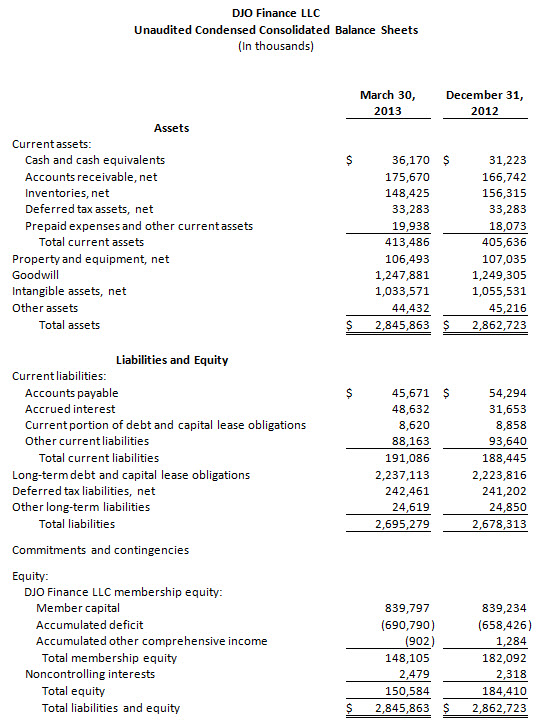

As of March 30, 2013, the Company had cash balances of $36.2 million and available liquidity of $82 million under its revolving line of credit. During the first quarter of 2013, the Company amended its senior secured credit facility to, among other things, reduce the interest rate applicable on the term loans outstanding under the senior secured credit facility to LIBOR plus 3.75%, subject to a minimum LIBOR rate of 1.00%.

Conference Call Information

DJO has scheduled a conference call to discuss this announcement beginning at 1:00 pm, Eastern Time today, April 26, 2013. Individuals interested in listening to the conference call may do so by dialing (866) 394-8509 (International callers please use (706) 643-6833), using the reservation code 22322226. A telephone replay will be available for 48 hours following the conclusion of the call by dialing (855) 859-2056 and using the above reservation code. The live conference call and replay will be available via the Internet at www.DJOglobal.com.

About DJO Global

DJO Global is a leading global developer, manufacturer and distributor of high-quality medical devices that provide solutions for musculoskeletal health, vascular health and pain management. The Company’s products address the continuum of patient care from injury prevention to rehabilitation after surgery, injury or from degenerative disease, enabling people to regain or maintain their natural motion. Its products are used by orthopedic specialists, spine surgeons, primary care physicians, pain management specialists, physical therapists, podiatrists, chiropractors, athletic trainers and other healthcare professionals. In addition, many of the Company’s medical devices and related accessories are used by athletes and patients for injury prevention and at-home physical therapy treatment. The Company’s product lines include rigid and soft orthopedic bracing, hot and cold therapy, bone growth stimulators, vascular therapy systems and compression garments, therapeutic shoes and inserts, electrical stimulators used for pain management and physical therapy products. The Company’s surgical division offers a comprehensive suite of reconstructive joint products for the hip, knee and shoulder. DJO Global’s products are marketed under a portfolio of brands including Aircast®, Chattanooga, CMF™, Compex®, DonJoy®, Empi®, ProCare®, DJO® Surgical, Dr. Comfort® and ExosTM, For additional information on the Company, please visit www.DJOglobal.com.

Safe Harbor Statement

This press release contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. Such statements relate to, among other things, the Company’s expectations for its growth in revenue and Adjusted EBITDA and its opportunities to improve commercial execution and to develop new products and services. The words “believe,” “will,” “should,” “expect,” ”target,” “intend,” “estimate” and “anticipate,” variations of such words and similar expressions identify forward-looking statements, but their absence does not mean that a statement is not a forward-looking statement. These forward-looking statements are based on the Company’s current expectations and are subject to a number of risks, uncertainties and assumptions, many of which are beyond the Company’s ability to control or predict. The Company undertakes no obligation to update any forward-looking statements, whether as a result of new information, future events or otherwise. The important factors that could cause actual operating results to differ significantly from those expressed or implied by such forward-looking statements include, but are not limited to: the successful execution of the Company’s business strategies relative to its Bracing and Vascular, Recovery Sciences, International and Surgical Implant segments; the continued growth of the markets the Company addresses and any impact on these markets from changes in global economic conditions; the successful execution of the Company’s sales and acquisition strategies; the impact of potential reductions in reimbursement levels and coverage by Medicare and other governmental and commercial payors; the Company’s highly leveraged financial position; the Company’s ability to successfully develop, license or acquire, and timely introduce and market new products or product enhancements; risks relating to the Company’s international operations; resources needed and risks involved in complying with government regulations; the availability and sufficiency of insurance coverage for pending and future product liability claims, including multiple lawsuits related to the Company’s cold therapy products and its discontinued pain pump business; and the effects of healthcare reform, Medicare competitive bidding, managed care and buying groups on the prices of the Company’s products. These and other risk factors related to DJO are detailed in the Company’s Annual Report on Form 10-K for the year ended December 31, 2012, filed with the Securities and Exchange Commission on February 28, 2013. Many of the factors that will determine the outcome of the subject matter of this press release are beyond the Company’s ability to control or predict.

DJO Finance LLC

Adjusted EBITDA

For the Three Months Ended March 30, 2013 and March 31, 2012

(unaudited)

Our Amended Senior Secured Credit Facility, consisting of a $859.9 million term loan and a $100.0 million revolving credit facility, under which $18.0 million was outstanding as of March 30, 2013, and the Indentures governing our $330.0 million of 8.75% second priority senior secured notes, $440.0 million of 9.875% senior notes, $300.0 million of 7.75% senior notes, and $300.0 million of 9.75% senior subordinated notes represent significant components of our capital structure. Under our Amended Senior Secured Credit Facility, we are required to maintain specified first lien net leverage ratios, which become more restrictive over time, and which are determined based on our Adjusted EBITDA. If we fail to comply with the first lien net leverage ratio under our Amended Senior Secured Credit Facility, we would be in default. Upon the occurrence of an event of default under the Amended Senior Secured Credit Facility, the lenders could elect to declare all amounts outstanding under the Amended Senior Secured Credit Facility to be immediately due and payable and terminate all commitments to extend further credit. If we were unable to repay those amounts, the lenders under the Amended Senior Secured Credit Facility could proceed against the collateral granted to them to secure that indebtedness. We have pledged a significant portion of our assets as collateral under the Amended Senior Secured Credit Facility. Any acceleration under the Amended Senior Secured Credit Facility would also result in a default under the Indentures governing the notes, which could lead to the note holders electing to declare the principal, premium, if any, and interest on the then outstanding notes immediately due and payable. In addition, under the Indentures governing the notes, our ability to engage in activities such as incurring additional indebtedness, making investments, refinancing subordinated indebtedness, paying dividends and entering into certain merger transactions is governed, in part, by our ability to satisfy tests based on Adjusted EBITDA. Our ability to meet the covenants specified above will depend on future events, many of which are beyond our control, and we cannot assure you that we will meet those covenants.

Adjusted EBITDA is defined as net income (loss) attributable to DJO Finance LLC plus interest expense, net, income tax provision (benefit), and depreciation and amortization, further adjusted for certain non-cash items, non-recurring items and other adjustment items as permitted in calculating covenant compliance and other ratios under our Amended Senior Secured Credit Facility and the Indentures governing our 8.75% second priority senior secured notes, 9.875% senior notes, 7.75% senior notes and our 9.75% senior subordinated notes. We believe that the presentation of Adjusted EBITDA is appropriate to provide additional information to investors about the calculation of, and compliance with, certain financial covenants and other ratios in our Amended Senior Secured Credit Facility and the Indentures. Adjusted EBITDA is a material component of these calculations.

Adjusted EBITDA should not be considered as an alternative to net income (loss) or other performance measures presented in accordance with accounting principles generally accepted in the United States of America (“GAAP”), or as an alternative to cash flow from operations as a measure of our liquidity. Adjusted EBITDA does not represent net income (loss) or cash flow from operations as those terms are defined by GAAP and does not necessarily indicate whether cash flows will be sufficient to fund cash needs. In particular, the definition of Adjusted EBITDA under our Amended Senior Secured Credit Facility and the Indentures allows us to add back certain non-cash, extraordinary, unusual or non-recurring charges that are deducted in calculating net income (loss). However, these are expenses that may recur, vary greatly and are difficult to predict. While Adjusted EBITDA and similar measures are frequently used as measures of operations and the ability to meet debt service requirements, Adjusted EBITDA is not necessarily comparable to other similarly titled captions of other companies due to the potential inconsistencies in the method of calculation.

The following table provides reconciliation between net loss and Adjusted EBITDA:

(1) Consists of direct acquisition costs and integration expenses related to acquired businesses and costs related to potential acquisitions.

(2) For the twelve months ended March 30, 2013, litigation and regulatory costs consisted of $2.8 million of estimated costs to complete a post-market surveillance study required by the FDA related to our discontinued metal-on-metal hip implant products, $4.5 million in litigation costs related to ongoing product liability issues related to our discontinued pain pump products, a $1.3 million judgement related to a French litigation matter we intend to appeal and $3.8 million related to other litigation and regulatory costs and settlements.

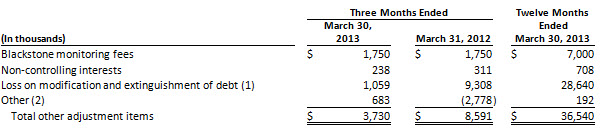

(c) Other adjustment items are comprised of the following:

(1) Loss on modification and extinguishment of debt for the three months ending March 30, 2013 consists of $0.9 million in arrangement and amendment fees and other fees and expenses incurred in connection with the amendment of our senior secured credit facilities and $0.2 million related to the non-cash write off of unamortized debt issuance costs and original issue discount associated with term loans which were extinguished. Loss on modification and extinguishment of debt for the twelve months ending March 30, 2013 consists of the preceding amounts and $17.2 million in premiums related to the repurchase or redemption of our 10.875% Notes, $12.7 million related to the non-cash write off of unamortized debt issuance costs related to the 10.875% Notes and $0.1 million in legal and other fees, net of $2.5 million related to the non-cash write off of unamortized original issue premium associated with the 10.875% Notes. Loss on modification and extinguishment of debt for the three months ending March 31, 2012 consists of $8.5 million of arrangement and amendment fees and other fees and expenses incurred in connection with the March 2012 amendment of our Senior Secured Credit Facility and $0.8 million related to the non-cash write off of unamortized debt issuance costs and original issue discount associated with a portion of our term loans which were extinguished.

(2) Other adjustments consist primarily of net realized and unrealized foreign currency transaction gains and losses.

(d) Other adjustment items applicable for the twelve month period include future cost savings and pre-acquisition EBITDA for the twelve months ended March 30, 2013 related to the acquisition of Exos Corporation.